Anchoring inflation expectations is one of the prerequisites for achieving price stability. In an environment where expectations are anchored, inflation expectations converge to the central banks’ inflation targets, the volatility of expectations wanes over time and differing expectations of survey participants converge to each other. The Central Bank of the Republic of Türkiye (CBRT) formulates its forward-looking forecasting path and sets its monetary stance in view of these measures in addition to the level of expectations. In this blog post, we share our findings on the anchoring of inflation expectations through the inflation expectations of market participants, firms and households in Türkiye.

To measure anchoring, we first calculate the rolling standard deviation of 12-month-ahead inflation expectations in the Survey of Market Participants (SMP) from the CBRT inflation forecasts.[1] Then, we measure the volatility of these expectations over time as well as the dispersion of expectations among survey participants.[2] Lastly, we derive a composite indicator to evaluate these anchoring measures, each of which provides different information. In addition, we calculate the composite indicator for firms and households using the data from the Business Tendency Survey (BTS) and Consumer Tendency Survey (CTS).

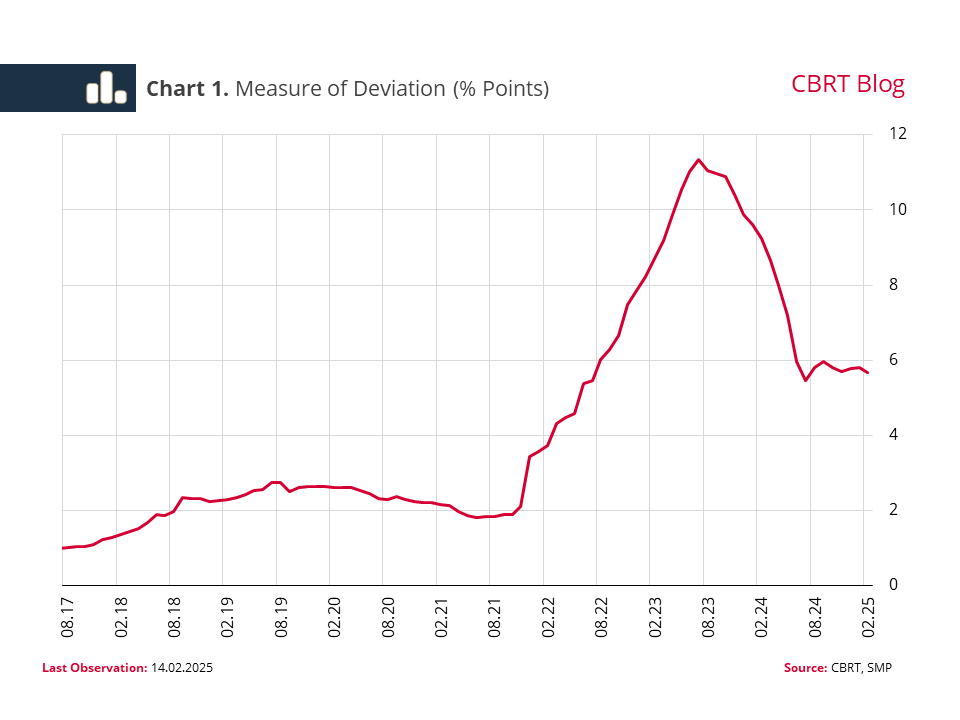

The first measure indicating the average level of divergence between inflation expectations of market participants and the CBRT forecasts reveals a decline in the deviation starting from the second half of 2023 and exhibits a flat course since the second half of 2024 (Chart 1).

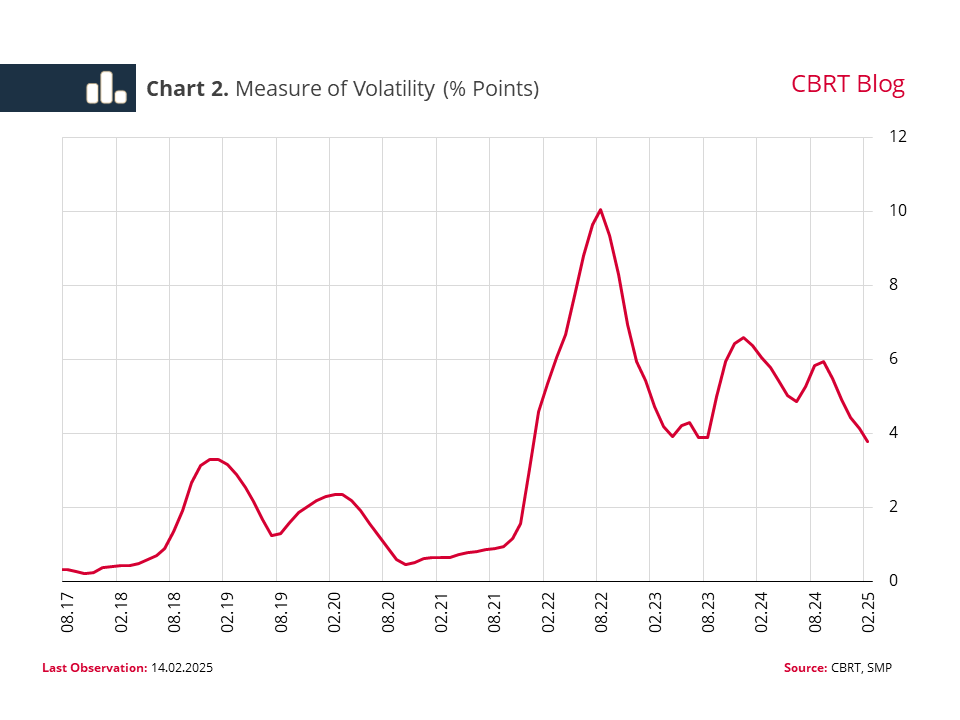

In a high inflation environment where pricing behavior has deteriorated, expectations may be subject to more frequent revisions. In such periods, the volatility of expectations over time, the second anchoring measure, assumes higher importance. It should also be noted here that in a high inflation environment, a decline in volatility alone may not be sufficient for anchoring. Volatility may increase in periods when the monetary policy stance changes, while it may diminish in periods when expectations become rigid. Meanwhile, the measure of volatility has recently settled on a downward trend (Chart 2).

Dispersion, another anchoring measure, shows the extent of proximity of forecasts among different participants. Increasing consensus among survey participants boosts the anchoring of expectations. This measure suggests a significant fall in dispersion over time, which results in convergence of expectations of different participants over time (Chart 3).

Although the above-mentioned measures address the anchoring of expectations from different perspectives, interpreting these measures separately may not be sufficient to measure anchoring. Therefore, we create a composite anchoring indicator as equal weighted average of the deviation of expectations from official forecasts, the volatility of expectations over time and the divergence among participants' expectations. This composite indicator reveals that anchoring of expectations, which weakened as of the last quarter of 2021, has gradually improved under tight monetary policy (Chart 4).

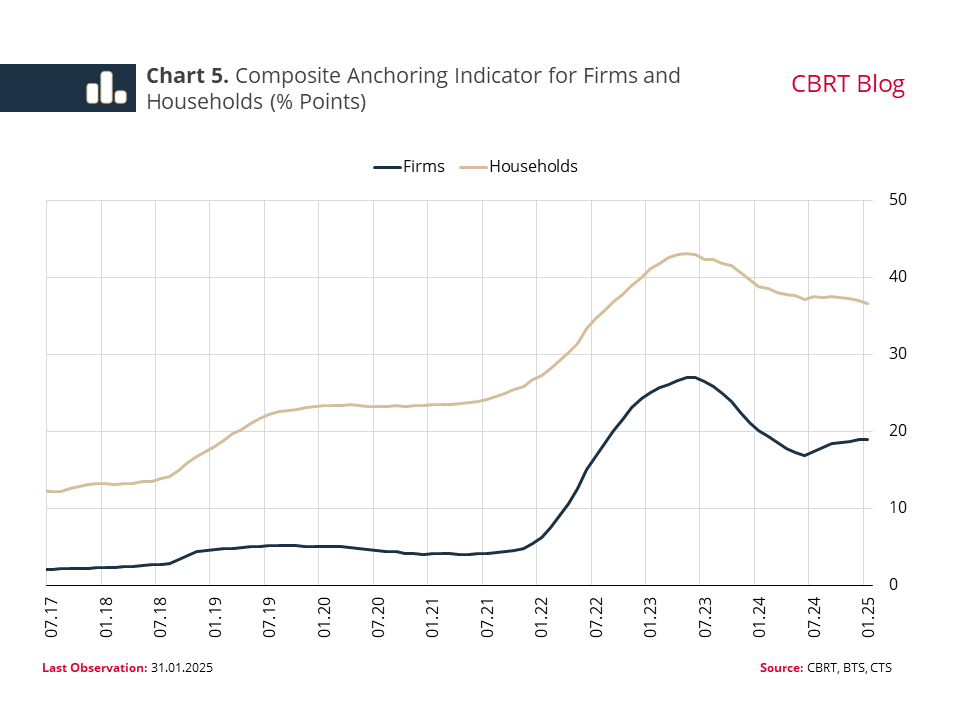

On the one hand, it is documented that inflation expectations of households and firms are systematically biased upwards, dispersed and volatile compared to market participants.[3] On the other hand, similar to market participants, inflation expectations of firms and households also tend to be anchored. The composite anchoring indicator, which starts deteriorating for both groups in the end of 2021, has recovered since the summer of 2023 (Chart 5).

In sum, on the back of the tight monetary policy adopted as of the second half of 2023, both the level and distribution of inflation expectations have improved. Sustained recovery in anchoring measures in the upcoming period will underpin efforts to achieve and maintain price stability.

[1] All measures are calculated by 12-month moving windows for 12-month-ahead expectations.

[2] For additional information on the anchoring measures used in the blog post, see: Bems et al. (2021). “Expectations' anchoring and inflation persistence”. Journal of International Economics, 132, 103516.

[3] For details, see: D'Acunto et al. (2023). “What do the data tell us about inflation expectations?”. In Handbook of economic expectations (pp. 133-161) and Andre et al. (2021) “Inflation Narratives”, CEPR Discussion Paper 16758.